The loan process can be scary, especially if you don’t know what you’re signing up for. Whether you are an investor or a lender, think about what kind of agreement you will use to spell out the terms of your loan. Most of the time, lenders will start having a conversation with clients about their agreement, which comprises one or two papers.

The first is a promissory note, and the second is a loan agreement. You should know the difference between the two to tell them apart. Whether you use a promissory note format or a loan agreement, you must ensure it is accurate and shows what both sides want. Let’s understand in detail what a promissory note and a loan agreement are.

What is a Promissory Note?

A promissory note is when one person gives in writing a promise to pay another person a set amount of money immediately or on a specific date. A promissory note includes essential details, including the amount of debt, interest rate, and maturity date. It also outlines the payment plan, the date and place of issue, and the issuer’s name.

Promissory notes can be somewhere between an IOU or I owe you and a loan contract, regardless of how serious or informal they are. An IOU only confirms that someone owes money to someone else and how much they owe. A promissory note details the steps required to return the debt, such as the payback plan, and includes a promise to pay on demand or at a specific date.

Things to Keep In Mind While Writing a Promissory Note

A formal agreement is always preferable when lending or borrowing money. You can use a promissory note format, a formal document that spells out the terms of a loan, like when the money is due and how much interest is charged. Consider some things if you want to write a promissory note to ensure it is legally binding and effective.

Read More:

Gather Necessary Information

It is essential to get all the information you need before making a promissory note. This includes the full name of the parties to the agreement, contact information, loan amount, interest rate, and due date. Also, include any collateral that will be used to secure the loan and any fees that will be charged for not paying on time or not paying at all.

If you’re going to explain the loan terms, you should be very clear. This will help keep things clear in the future. When you say that the loan must be paid back in monthly installments, for example, you should be more specific about how much each payment is and when it is due.

Pick the Right File Format

When writing a promissory note, you can use different styles. You can always write it yourself or use a template. If you choose to write the note yourself, use simple, clear language that is easy to understand. Don’t use legal language or terms that are too complex for the customer to understand.

Before using it, make sure your chosen style suits your needs. Although the Internet has many free promissory note format samples, not all may be valid in your area. Do some research to ensure the template you pick meets all the legal requirements.

Read More: Understanding 8 Possible Risks of Unsecured Personal Loans

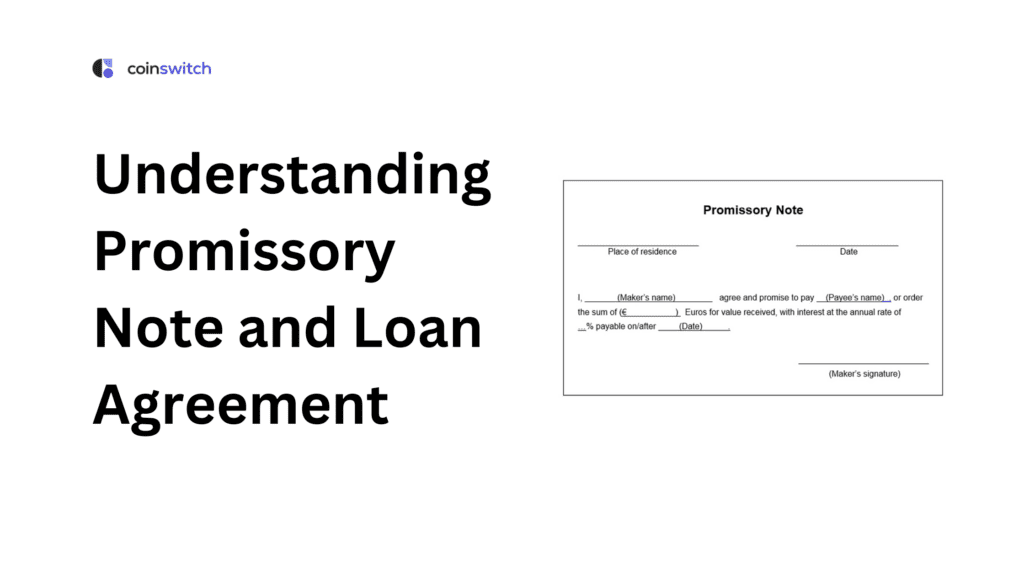

Sample Promissory Note Format

Sample

Promissory Note

Principal amount: $ [amount of loan]. Due date: [date]

This is [borrower’s name], and my street address is [city], [province], [postal code]. I promise to pay [payee’s name], who also lives at [street address] in [city], [province], [postal code], the amount of [amount of loan] dollars.

The amount still owed will have interest added to it at a rate of [interest rate] % per year.

You’ll be charged extra money if you don’t pay within [number] days of the due date. The late charge will be added to the balance.

To be paid at [city], [province], on [date].

SIGNED on [date] in the city of [city].

———————————

Signature of a witness

———————————

Signed by the borrower

———————————

Name of witness

———————————

Name of borrower

———————————

Address of a witness

———————————

Signed date

What is a Loan Agreement?

A loan agreement is a legally binding contract between a lender and a borrower that spells out how the money will be disbursed and paid back. These deals are often linked to mortgages, but banks and other financial companies also use them when giving large amounts of money for different reasons. Unlike the usual promissory note format, a loan agreement, which usually runs into more than one page, spells out essential details like the due date, interest rates, and late payment fees.

It also states what can happen if the user doesn’t repay the loan. The deal is usually made using strict and formal wording to keep things simple and in line with the law. This is why borrowers need to get professional help before signing. Carefully reading the terms can help avoid confusion, prevent hidden costs, and ensure that both parties fully understand their responsibilities under the contract.

Simple Loan Agreement Sample/Template

It is important to have a clear and legally viable loan agreement, which would help in avoiding serious misunderstandings. The right format would provide a framework within which any disputes can be resolved. Here is a template-

Sample

LOAN AGREEMENT

PARTIES

This Loan Agreement was made on (the “Effective Date”) by and between (the “Borrower”) and (the “Lender”), who are (collectively called the “Parties”).

INFORMATION

Both sides agree to put their basic facts below: Your name, address, email address, phone number, the phone numbers of two references, and the things you are lending money against as protection and collateral.

The Lender’s name, location, email address, and phone number are: ——-

LOAN

The parties agree that the information below about the loan is correct.

Date when the first payment is due: ————–

Date the last payment is due: ——————–

Amount of the loan: ——————

Rate of Interest: —————–

Fee for being late: ——————–

How to Pay: —————–

Tax Implications on Loans between Friends/Relatives

The seller or the user does not pay tax on loans without interest. If the provider charges interest, they must list it as Income from Other Sources in their income tax return. People who take money from friends, family, or non-financial companies to build a house can’t claim the payments on their taxes.

In this case, Section 80C doesn’t offer any help with paying back the debt. Under Section 24 of the Income Tax Act, you can claim a tax credit for the interest you paid on the loan, as long as the money was used to build a house. The main requirement is that the loan be used for real estate-related things.

Opinion on Lending Money to Friends or Relatives

Lending money to friends or relatives in India is an emotional decision and not a financially prudent one. Although one might think that assisting a loved one who is in need is the right thing to do, it can put a strain on relationships when the person defaults or is slow at repaying the loan. In most situations, it is informal, but it is complicated under the law.

In addition, when the amount involved is huge, it may affect your personal financial stability. It is best to agree on the terms of repayment beforehand. Also, it is necessary to find the balance between empathy and prudence.

Conclusion

Loan agreements and promissory notes are important legal documents that spell out the terms of lending and borrowing. People find promissory notes easier to understand for smaller amounts.

They often use them instead of loan agreements that have more specific terms. Banks usually use the promissory note format, but other groups or people can also use it to confirm the terms of a loan agreement. Picking the proper document clarifies things, protects you legally, and speeds up financial activities.

FAQs

1. What is the difference between a promissory note and a loan agreement?

A loan agreement is a written contract outlining the terms the borrower and the lender agreed upon. In a promissory note format, one party writes down their promise to pay another party a certain amount of money as agreed.

2. What are the details of the promissory note?

A promissory note format must include the loan amount, the loan date, the seller’s and the borrower’s names, the interest rate, and the due date. When both sides sign the paper, it becomes a legally binding agreement.

3. Do you need a promissory note with a loan agreement?

Loan agreements are better for complicated cases involving larger amounts of money, while the promissory note format is better for smaller, less formal, and unprotected loans. However, lenders and borrowers may want to include both a written note and a loan agreement occasionally.

4. What is the difference between a loan note and a loan agreement?

A loan note is a shorter document that only discusses the loan basics, while a loan agreement is more extensive and covers all the loan details. Another critical difference is that the amount of legal protection each paper provides is different.